Caterpillar Inc. is a manufacturer of construction and mining equipment, diesel & natural gas engines, industrial gas turbines & diesel-electric locomotives. Its segments include Resource Industries, Construction Industries and Power Systems. It is highly linked to the mining and home construction industries.

-Seven Year Revenue Growth Rate: 3.78%

-Seven Year EPS Growth Rate: 2.61%

-Seven Year Dividend Growth Rate: 12.84%

-Current Dividend Yield: 3.17%

-Seven Year EPS Growth Rate: 2.61%

-Seven Year Dividend Growth Rate: 12.84%

-Current Dividend Yield: 3.17%

Overview

While the US housing construction industry finally came back from the dead, the mining industry is falling into a deep sleep due to the lack of demand. Emerging markets are not so emerging anymore and their appetite for resources has slowed down. But this is short term news. The truth is that CAT is highly diversified among the mining, construction & energy and transportation industries. Global energy demand growth will continue to sustain the E&T division while construction won’t slow in the States anytime soon. Since sales and profits have declined over the past 12 months, CAT has tightened its control over inventory and costs. The company is now leaner and stronger. The demand for resources will reappear at one point and the mining industry will benefit from it. CAT is the leader in mining equipment; it will get its share of the cake at that point.

While CAT is a very strong pick for a long term perspective, it might be riskier over a short period such as 12 months. If the mining industry continues to slow down as is the case right now, CAT might not be able to meet its double digit growth projection. For that reason, I think you should take a careful look at this company before going forward.

Ratios

Price to Earnings: 14.17

Price to Free Cash Flow: 13.46

Price to Book: 3.145

Return on Equity: 20.73%

Price to Free Cash Flow: 13.46

Price to Book: 3.145

Return on Equity: 20.73%

Revenue

As previously mentioned, Caterpillar is suffering from the global economic slowdown for resources. Low oil prices reduce the demand for drilling equipment. Then, emerging markets appetite for resources has seriously declined leading the mining industry downward. The US construction environment is doing well, supporting Caterpillar’s revenue at the moment. However, we don’t expect much growth in the upcoming year. CAT is a cyclical company evolving in a tough market at the moment. It may be the right time to invest. Let’s take a look at others metrics.

Earnings and Dividends

Throughout the years, I’ve built a serious investing model including 7 rules of investing. These rules were built based on much stock researches and my 13 years as an investor. Here’s the first rule:

#1 High Dividend Yield Doesn’t Equal High Returns

It has been proven that high yield dividend stocks (over 5%) underperform the market. It’s only normal as companies paying over 5% dividend yield show a high level of risk or limited growth potential when most money is simply redistributed to investors through dividends. Those companies (such as MLP’s) are good for retirees seeking income, but not really interesting for a young investor like me (I’m in my 30s). Let’s take a look at CAT’s dividend yield throughout the years;

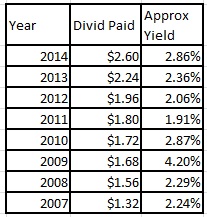

Approximate historical dividend yield at beginning of each year:

As you can see, CAT shows a relatively low dividend yield over the past 7 years but recently went over the 3% bar. This places CAT in a good position for dividend investors.

#2 If There is One Metric; It’s Dividend Growth

The second rule is quite simple, but really effective. If there is only one metric you should be looking at, it has to be the dividend growth. If a company grows its dividend year after year, it means profit and sales are also increasing.

While CAT is going through a tougher period at the moment, we can appreciate a strong annualized dividend growth of 12% over the past 5 years. Here again, the company fits my investing criteria.

#3 A Dividend Payment Today is Good, a Payment for the next 10 Years is Better

As previously mentioned; a company increasing its dividend payment year after year must also show revenue and profit growth to sustain its distribution. A good way to see if the company can make it through the next 10 years is to look how the payout ratio has evolved through time. In the previous graph, we see a payout ratio under 50% for the past 4 years. This is a very good indication that the dividend is sustainable.

#4 The Foundation of Dividend Growth Lies in its Business Model

Warren Buffet once said he invests only in businesses he understands. This is crucial to making rational investment decisions. Caterpillar’s economic moat is quite interesting. This business is selling world class equipment for various industries.

The company evolves in cyclical markets and revenues and profits fluctuate over time. However, it’s a leader in its industry and the quality of its equipment is well appreciated around the world.

How Does CAT Spend Its Cash?

The company has well defined priorities for its cash flow:

#1 Maintain financial strength

#2 Growth

#3 Pensions

#4 Dividends

#5 Stock Repurchases

This quote from their last earnings call with management resumes how CAT manages its cash flow:

Risks

While CAT is a very strong pick for a long term perspective, it might be riskier over a short period such as 12 months. If the mining industry continues to slow down as is the case right now, CAT might not be able to meet its double digit growth projection. For that reason, I think you should take a careful look at this company before going forward.

The company currently focuses on cost management to maintain its profit while waiting for the next resource driven wave to improve its results.

Conclusion and Valuation

The first valuation method used is a look at the historical PE ratio. It gives me an idea of how the market values the company:

Due to the economic slowdown, we see CAT losing strength in the valuation multiplier. Not so long ago, the company traded around 18 but it is now back to 14 times the benefits. The company seems slightly undervalued using the PE historic method. Let’s see what it looks like with the Dividend Discount Model:

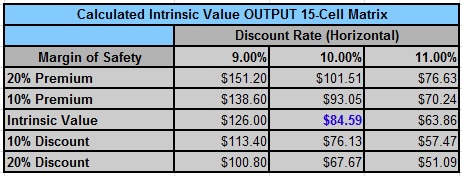

Considering a 10 year dividend growth of 5% (considering the current market headwind) and a 7% average dividend growth rate for the future, we get a fair value at $84.59 while the stock is currently trading at $88-$89. I’ve used a discount rate of 10% as the company is very stable and will continue to be a leader in its industry.

In the light of both valuation methods; I can say Caterpillar is a good addition to a portfolio at the current price. What do you think?

Source: DividendMonk.com.

No comments:

Post a Comment